Stock story: Ridley

A company with a strong return tells you how well it has done with the capital already invested in it, but what matters just as much is the return it earns on the next dollar. This is referred to as the incremental return on capital, and over time it is what separates a business that keeps compounding value from one that destroys value. This factor is, in our view, one of the least appreciated figures in the market and can lead to tremendous shareholder returns.

Identifying these businesses is not as simple as screening for high returns, because a screen looks backwards and the shift we are looking for shows up in the return on new capital well before it moves the blended return the market fixates on. How we look for these businesses often revolves around finding a key catalyst that has played out and which the market is yet to fully appreciate. It might be a change in industry regulation that reshapes the competitive landscape, a reduction in competition as an irrational player exits the market or industry consolidation occurs or a change in management or the board that finally brings discipline to how capital is allocated.

In each case, the effect is the same: the next dollar invested starts earning more than the last, whether that lifts an already strong business higher or drags a weaker one back towards respectability. Underpinning all of it, though, must be a sound balance sheet, the one thing we are not prepared to compromise on. Too much debt removes a company’s flexibility, forcing it to cut investment or sell assets at the worst possible moment, whereas financial strength buys management the time to reinvest patiently and ensures the rewards ultimately accrue to shareholders.

The difficulty in identifying these businesses is what creates the opportunity. The market anchors to a company’s history; it is slow to pay for returns that are only beginning to shift. That can leave a genuinely good business at an undemanding price. The appeal of buying these businesses is that value can accrue from two directions at once, with both the improving incremental returns lifting earnings, and the market gradually recognising the shift and affording the business a higher multiple. It is this combination, a reasonable starting valuation paired with returns that are quietly compounding higher, that we find most compelling, and it is rarely on offer in businesses whose quality is already obvious to everyone.

A recent addition to our portfolio that we feel illustrates these high incremental returns is Ridley Corporation (RIC.AX). Ridley is the country’s largest supplier of animal nutrition, providing feed for everything from livestock to poultry to aquaculture. It is an essential, unglamorous operation with entrenched customer relationships and a national footprint that would be difficult and expensive to replicate. Yet for years its returns did not reflect the quality of the assets, weighed down by capital that had been committed in the wrong areas. Looking only at its history, an investor could be forgiven for concluding this was a mediocre business. We would argue it was simply a good business that had been run without enough attention to where its incremental capital was going.

The catalyst, as it so often is, was a change at the top. The appointment of Quinton Hildebrand as Chief Executive Officer in 2019, followed by Mick McMahon as Chairman in 2020, brought a sharper focus on returns and a willingness to question the capital the business had inherited. Crucially, the new team members had no attachment to the decisions of the past and were therefore free to judge each asset on the return it actually earned rather than on the reason it had been built.

They went to work on the capital base from both ends, removing what was destroying value and reshaping what could create it. The clearest example of the former was the Westbury extrusion facility in Tasmania, constructed under prior management at considerable cost and in a competitive market. Quinton, who had not built it, felt no obligation to keep it, and the business sold the facility shortly after it was constructed. This allowed the capital to be reallocated into higher-returning ventures and repaired the balance sheet.

This reallocation of capital into higher-returning ventures is clearest in the bulk stockfeed segment. Feedmills are a business of fixed costs and utilisation: a mill running below capacity earns poor returns, while one running full is highly profitable, because each extra tonne of feed adds very little incremental cost. Rather than protect margins by holding prices high and accepting under-utilised mills, management did the counter-intuitive thing and lowered prices. The lower prices won volume, that volume filled the mills, and the improvement in utilisation more than paid for the price given up, while also providing a stronger moat, as it was difficult for competitors with lower market share to match these prices.

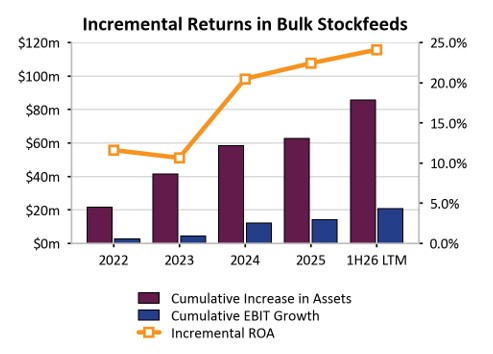

Only once the mills were full did they add capacity, with capacity expansion underwritten by customers. Because that new capacity was spoken for before it was built, it ran at high utilisation from day one and earned an attractive return on the incremental dollar almost immediately. Better still, they passed the benefits of greater scale back to the customers through lower prices, deepening those relationships and reinforcing the loyalty that underwrites the next round of expansion. One of our favourite books on investing, William Green’s Richer, Wiser, Happier, attributed this concept of “scale economies shared” to global investor Nicholas Sleep. We usually expect to see this in successful category-killer retailers (indeed, it is the dynamic underpinning the success of portfolio holding Sigma Healthcare via Chemist Warehouse). We do not usually expect to see the “scale economies shared” dynamic in animal feed! It is a virtuous circle, and it shows up directly in the incremental returns the division now earns. From 2022 to 1H 2026, management added c. $80 million in incremental assets to the division. This asset investment saw a cumulative $20 million in incremental earnings added to the division, representing a cumulative ROIC of around 25% – well above both the segment and group returns.

Source: Company Accounts

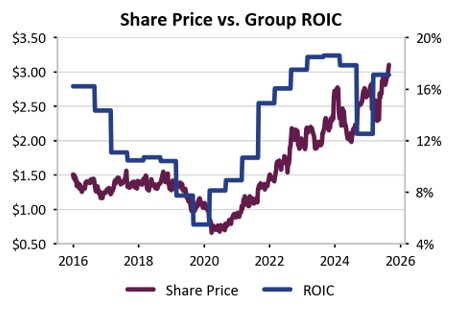

This is precisely what investors should be looking for, and yet it is rarely obvious in the headline numbers while it is happening. A business that grows its returns is a business earning more on every new dollar it invests, and over time that is what drives the value of the company. The market eventually recognises this, but it tends to do so with a lag, which is why the share price so often ends up tracking the group returns rather than anticipating its improvement.

Source: Refinitiv; Company Accounts

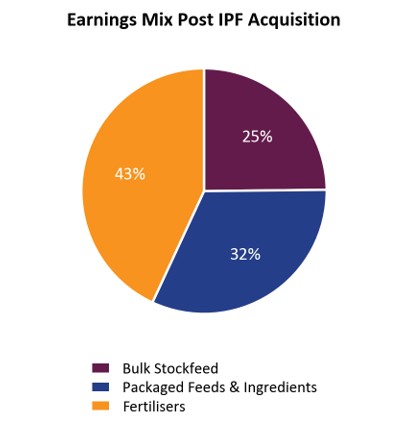

We see scope for this improvement to continue following the acquisition of Incitec Pivot Fertilisers (IPF) in 2025. IPF is Australia’s largest fertiliser distribution business, and one that had been unloved and underinvested in by its previous owner. This is the same playbook running in reverse: rather than selling a poor asset, the team is buying one cheaply and setting about lifting its returns. Indeed, Ridley bought IPF so cheaply that it had to recognise an accounting gain on acquisition in its P&L – a sign that the business was acquired for less than the value of its working capital. Having already shown, in both aquafeed and stockfeed, that they know how to allocate capital well, we think they can do the same with IPF.

The early signs are encouraging. Ridley has appointed a new Chief Financial Officer, Chris Opperman, previously the CFO of IPF, who understands the business intimately and knows where capital can be invested to improve returns. The acquisition is also meaningful in scale, with the fertiliser division making up around 40 per cent of group earnings, so even a modest lift in its returns would move the needle for the group as a whole.

Source: Company Accounts

It is exactly the combination we look for with Ridley having an extremely hard-to-replicate network of assets, a management team that has earned our trust on capital allocation, and a valuation that still reflects the returns of the past rather than the returns to come.

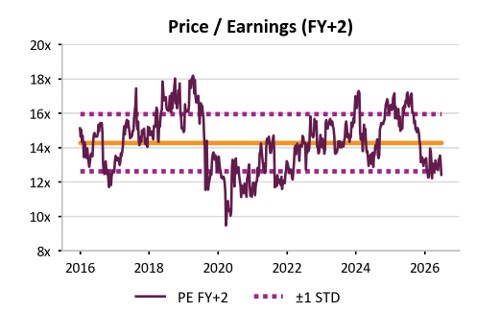

As the chart below shows, Ridley trades on a two-year forward price-to-earnings multiple of around one standard deviation below its ten-year average, despite a stronger management team, materially better returns, and a sizeable opportunity still ahead of it in lifting the returns of IPF. In our view the market is anchoring to the business Ridley used to be, rather than the one it is becoming, and that gap is where we believe the opportunity lies.

Source: Refinitiv

David Meehan

Equities Analyst

Important Information: Units in the fund referred to herein are issued by Magellan Asset Management Limited ABN 31 120 593 946, AFS Licence No. 304 301 trading as Magellan Investment Partners (‘Magellan’). This material is issued by Magellan and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to the relevant Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellaninvestmentpartners.com.

Past performance is not necessarily indicative of future results and no person guarantees the future performance of the fund, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan or the third party responsible for making those statements (as relevant). Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. This material may contain ‘forward-looking statements’. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third-party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan.

Further information regarding any benchmark referred to herein can be found at www.magellaninvestmentpartners.com/funds/benchmark-information/. (080825-#W14)